Maryland is actually a very interesting state when it comes to Medicare options, and how insurance carriers must do business here. When we look at Medicare in MD, we are going to break it down into a couple of categories.

How to Enroll in a Medicare Advantage Plan in Maryland

Table of Contents

In the state of Maryland, you will find that most folks on Medicare have a Medicare Supplement plan over a Medicare Advantage plan. While there are several reasons for this, we are going to start by looking at how the pricing is done by insurance carriers.

When you look at Medicare in MD, you will quickly see on the Medicare Supplement side that there is no area factoring allowed. Area factoring is a practice where an insurance company can charge more in premiums for those folks who live in what are known as high Medicare usage areas. This means that if you happen to live in a zip code where Medicare typically pays more in claims, then you will pay a higher premium for the exact same plan as someone who lives in a lower usage area.

In the state of Maryland, this practice is not allowed which means someone who lives in Baltimore, Maryland will pay the exact same price as someone who lives in Hagerstown, Maryland (same age, sex, and tobacco usage), Frederick, Maryland or even Cumberland, Maryland. It simply doesn’t matter where you live in Maryland because there is NO area factoring.

We are fortunate to have so many available insurance carriers in the state, which helps keep pricing quite competitive. Some of our favorite carriers offer great pricing on multiple plans. In addition to competitive premiums, most of the carriers also offer additional discounts such as a household discount which many times doesn’t even require both spouses to have a policy with that insurance company. This is beneficial when one spouse might have severe health issues that would keep them from being accepted by the new carrier, but still allows the healthier spouse to get the best pricing possible. In fact, several carriers have a household discount if there is simply another person living in the house with the policyholder who is over the age of 50. When looking at Medicare in MD you want to make sure that you are taking advantage of every possible discount that you can.

When looking at Medicare in MD you will quickly see that the amount of Medicare Supplement carriers far outpaces the amount of Medicare Advantage carriers.

Currently there are well over 30+ Medicare Supplement carriers doing business in the state of MD. With this many carriers available it allows us to find not only competitively priced plans, but also ones that have different levels of underwriting. The different levels of underwriting allow those folks with certain health conditions to find coverage as well. They might not qualify for one company due to their health condition, but another company may be fine with that condition.

While insurance companies can offer up to 10 standardized Medicare Supplement plans, most will elect to only offer 4-6 plans. Currently the most popular Medicare Supplement plans being purchased in Maryland are:

It is important to remember that only those Medicare beneficiaries whose effective dates for Part A and Part B was prior to January 1, 2020 can purchase a Plan F.

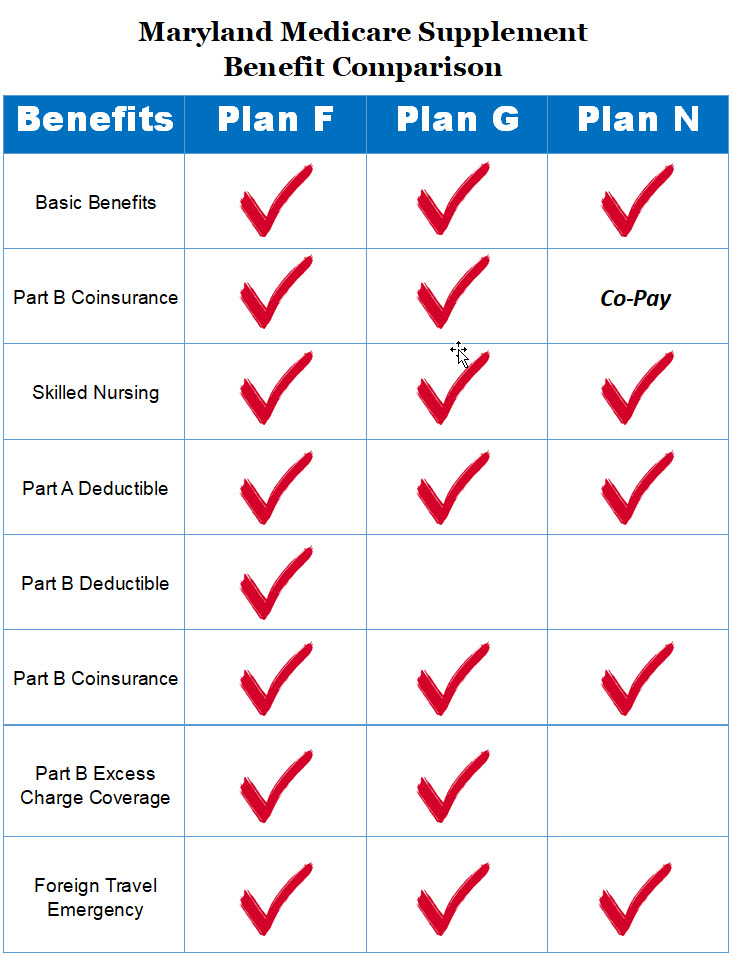

F Plan Benefits

G Plan Benefits

N Plan Benefits

Comparing a specific plan for a certain age often reveals monthly rates within a dollar of each other. An example of this would be for a 65-year-old female who is a non-tobacco user and wants a Plan G. You will notice that here in 2026 the rates are close to one another.

While Plan G is still one of the most popular plans in Maryland, the Plan N is also a favorite of those folks who want solid coverage but at even a lower monthly premium. Using the same criteria as we did above, here are the current monthly rates for 2026.

Keep in mind that the above rates do not factor in a household discount which can reduce premiums anywhere from 6% – 14% in Maryland.

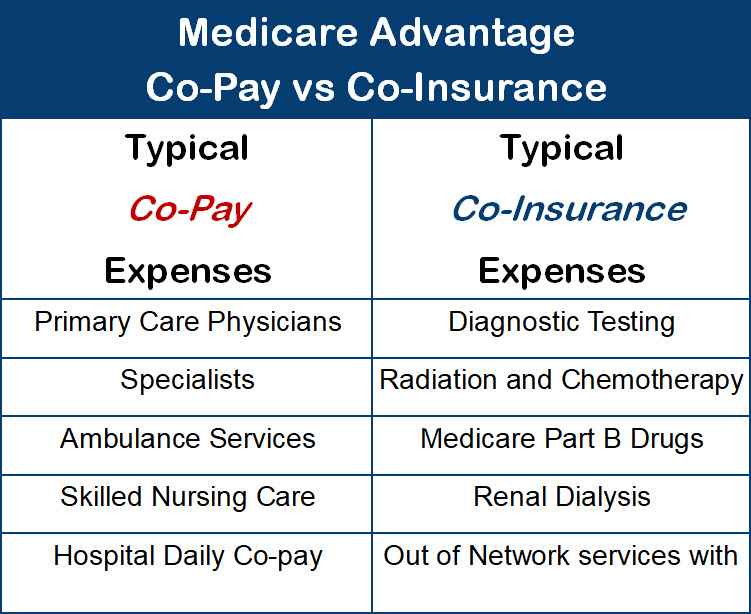

The state of Maryland does not have as many Medicare Advantage plans to choose from as other states. In Maryland, carriers with Medicare Advantage plans typically offer PPO or HMO networks. An HMO network restricts benefits, only paying providers within the network, while a PPO network allows coverage for payments to providers outside the plan’s network. These non-participating providers will still be paid at a lower rate, so there will be more out of pocket expenses for the policyholder to pay. When considering a Medicare Advantage plan it is very important to understand what services charge a co-pay and what services will be charged at a co-insurance amount. While one service might be a $20 co-pay, another service or procedure might be a 20% co-insurance payment. On a $1,000 charge, a 20% co-insurance would be $200.

Important areas to look at when considering a Medicare Advantage plan in addition to monthly premiums:

The number of carriers choosing to do Medicare Advantage business in Maryland differs by county. Yes, you read that correctly…they can limit their plan offerings to certain counties. Unlike Medicare Supplement plans that must be offered in all counties and be guaranteed renewable, a Medicare Advantage plan can be offered in as many as all counties or as few as just one. Also, Medicare Advantage plans are not guaranteed renewable which means that the plan can choose at the end of the contract year to exit the market in a particular county or even the whole state.

Plans by county/city:

Baltimore/Baltimore City – 6 carriers offering a total of 29 plans

Washington County/Hagerstown – 4 carriers offering a total of 16 plans

Frederick County/Thurmont – 6 carriers offering a total of 23 plans

Allegany County/Cumberland – 2 carriers offering a total of 8 plans

When you look at Medicare in Maryland you will see that there are far more choices for Medicare Supplement plans than Medicare Advantage Plans. This doesn’t necessarily mean that the Medicare Advantage plans are not beneficial to certain folks. It does mean that there are fewer choices and far less competition among them.

Hours :

Hours :

Hours :

Choices for Medicare in MD can be overwhelming, so don’t try going at it alone. Contact Senior Benefit Services, Inc to explore and understand all your options. Call us at (800)924-4727 and you will see how ‘We Make Medicare Easy’.

Hours :

Hours :

Hours :